Hello and welcome back to CRI's CTS Spotlight Blog.

08/17/12: In very

light holiday volume we have seen some dramatic price action through the

past week. Most notably, the much stronger US jobs data (and a waning

fear of recession) have put a top in the long dated government bonds and

have pushed major stock indices to within shouting distance of the

spring highs. The top in the 10 year US bond is so pronounced I have

made it the subject of this week's WCTS blog spotlight. Seeming to

confirm this 're-flation' notion, commodity prices in general are

moving higher across the board and most recent posts on being long the

commodity heavy TSX 60 and in some of the Softs markets all seem to be

working.

As we move our way through this 17.5 year 'fear' cycle (expected peak Q3, 2017) there ought to be a general preference towards income paying securities over growth [Please refer to CRI's Macro-economic analysis seminar for more detail]. The

fear of recession (both locally within North American and globally)

coupled with a credit crunch has had investors running to 'safe' assets,

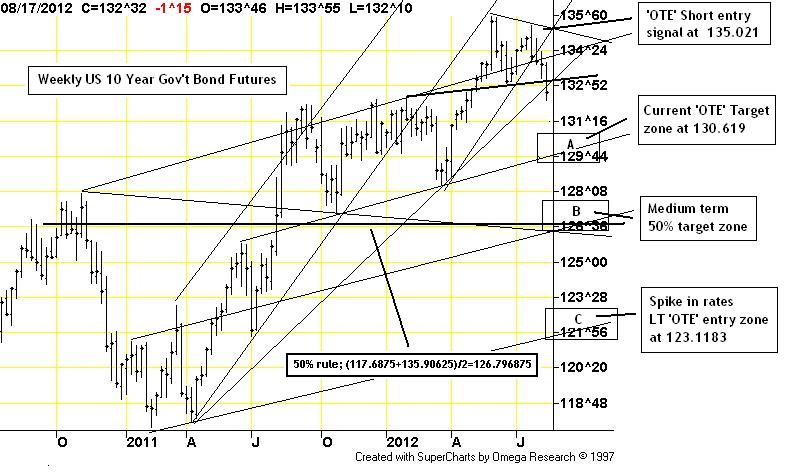

like US Government Bonds, for a few years now. This trend can be clearly seen in the chart above - where US Government Treasuries have enjoyed a rather dramatic bull run over the past few years.

While we know that this macro trend ought to continue for at least another five years, we also know that there ought to be pockets of 'correctionary' price action along the way. Short periods of time where the market cleans up any 'overbought' conditions before laying the groundwork for another leg higher. This is the point where I believe the market currently is. Not a new long term trend - a correction within a long term trend.

A rising bond market is in itself a deflationary situation - literally a lack of fear of inflation. The bursting of the US housing market bubble was the catalyst for the current 'dis-inflationary' spiral we are in now. Indeed, interest rates have move dramatically lower but may not clearly reflect the current situation. Economic data from North America is generally getting better as the FOMC has literally kept the gas pedal floored in an attempt to stimulate the economy. With the recent top in the bond market and an associated breakout to new highs in the stock market, one might come to be belief that the gas is finally reaching the engine.

So where might prices go over the near term if indeed there is a top in the bond market? The chart above clearly illustrates my three target zones should the recent top hold (please refer to chart above). These include a very healthy correction back into support around 130.6 (Point A.), a full correction back to the 50% level of this entire bull run around 126.80 (Point B.) and finally the 'all hell has broke loose' target back at the long term support around 123 (Point C.).

It is interesting to see that the US bond market set up an almost perfect 'OTE' short entry point around 135. It is interesting too that a move back to the refered to points above would represent interesting 'OTE' long entry areas.

That's all for this issue of the CTS Spotlight,

Brian Beamish FCSI

the_rational_investor@yahoo.com

the_rational_investor@yahoo.com