Hello and welcome back to CRI's CTS Spotlight Blog.

Since trading Crude Oil in earnest for the past six months (please refer to CRI's DayTradingBlog) I must admit I have been letting this blog slide a little of late.

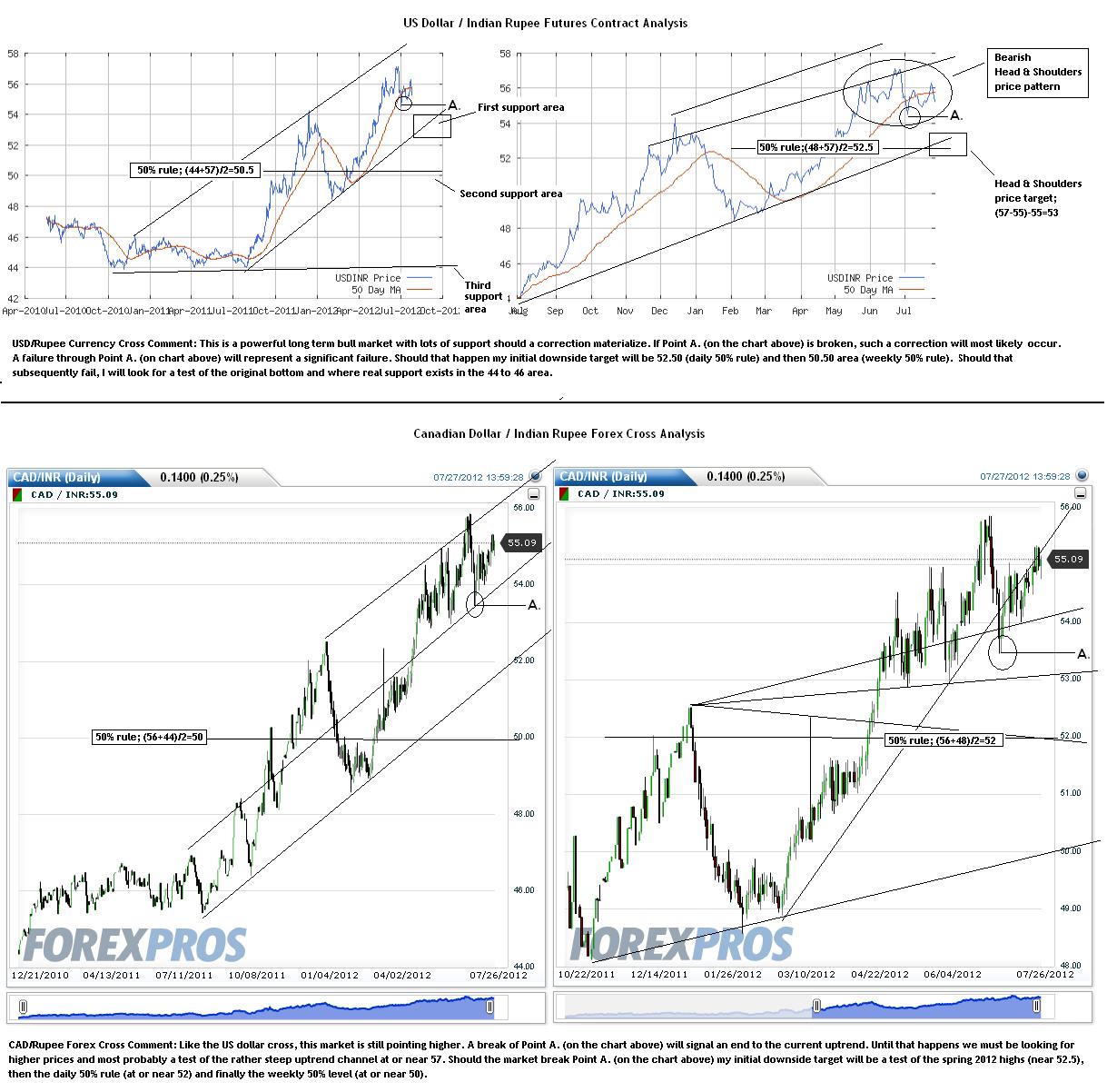

So for something a little different, I thought I might use this platform to take a look a specific markets as they come to my attention.To that end, this week a friend of mine asked for my thoughts on the Indian Rupee. Frankly, I have always been a little suspect of this currency trading unit and wouldn't be inclined to 'invest' my hard earned dollars into it directly. But considering the myriad of North American based ETF's and other such products, it seems only prudent to at least be cognizant of what is going on.

On first blush my knee jerk reaction was to be looking for a top. Yet one fatal mistake many novice traders do is to assume a change when there really isn't one. So, while my hunch is we need to come back to the daily and weekly 50% levels and clean up what appears to be an overbought market, there is NO top in place on either the US or Canadian crosses. One must still be looking for the recent highs to be tested and then if broken, the respective uptrend channel lines next.

On a side note, it is interesting to see such strength in the face what appears to be world wide weakness. This, in itself, is quite bullish and does suggest one ought to be looking for substantially higher prices to come. Is India becoming a reserve currency in itself? While that may be stretching things a bit, the internal Indian economy seems to be offsetting overseas weakness. While 'reserve currency' status may be years down the road, we at least know that for the next 5 years (give or take a quarter or two) this country will have the wind at its back and not in it's face...

Trading perspective. While this market is clearly trending higher, one must be weary of buying into risky markets. I could easily see the daily and weekly 50% levels tested in earnest and still feel like this market is trending higher. To that end, new purchases of either unit ought to be put on hold until some sort of 'clean up process' happens. Those that are long should be looking to take at least partial profits on existing positions (if you haven't already done so) and enjoying a free ride on the remaining (and what should be relatively 'risk free') positions.

That's all for this issue of the CTS Spotlight,

Brian Beamish FCSI

the_rational_investor@yahoo.com

the_rational_investor@yahoo.com