Hello and welcome back to CRI's CTS Spotlight Blog.

They say, when it rains it pours. To that end, here is yet another CTS Spotlight Blog entry for you to consider in the coming trading sessions.

There appears to be a general consensus on what to do about the European debt situation, how bad it really is and who could be potentially affected. There have also been very stern comments from the ECB suggesting they will do 'whatever is necessary' to defend the Euro-FX. Couple this 'capitulatory' talk with surprisingly bullish jobs data out of the US, a Fed ready to add liquidity (not take it away) and very robust corporate earnings and it is my belief that the late spring/early summer 2012 correction is behind us. Consider too that we do have an upcoming US Presidential election in early November. I only mention this last part because we very rarely have a collapsing market into such events.

From a contrarian perspecitive, it is Interesting to see that even though many of the world's indices are approaching their spring highs (and in my opinion starting to point higher in earnest) there remains a rather large bearish sentiment in the market - suggesting there are still plenty of investors either short or sitting on the sidelines. Should The Dow, Nasdaq or the S&P break to new highs, we could see a mass rush of buying on the 'don't miss the boat' trade.

From a contrarian perspecitive, it is Interesting to see that even though many of the world's indices are approaching their spring highs (and in my opinion starting to point higher in earnest) there remains a rather large bearish sentiment in the market - suggesting there are still plenty of investors either short or sitting on the sidelines. Should The Dow, Nasdaq or the S&P break to new highs, we could see a mass rush of buying on the 'don't miss the boat' trade.

So why am I mentioning all of this? Canadian stocks have been hit especially hard through this seasonal correction. Because of Canada's heavy reliance on the resource sector (a volatile sector by definition) Canadian investors have to face more and more volatility in their portfolios as we head into the 17.5 year 'fear' cycle peak. It's not much fun on the way down - but oh boy it can crazy on the way up. (which of course we all know exactly when it's gong to happen - right? If you answered NO to that question maybe you should go take CRI's macro-economics seminar to brush up on your fundamentals). Times ought to be very good for Canada in general over the next five years but any news/fear of recession in the US can/will lead to dramatic month-to-month price swings like we just saw over the past 4 months. Recent upbeat US jobs data, a very healthy yield curve and strong corporate profits are not the hallmarks of recessions and I do NOT believe the US is there at the moment. Once the US election is over and we are facing 'the fiscal cliff' I believe all bets are off and am probably going to suggest going to 'cash' at that point. But that is four months away and over the interim prices look to be heading higher - not lower.

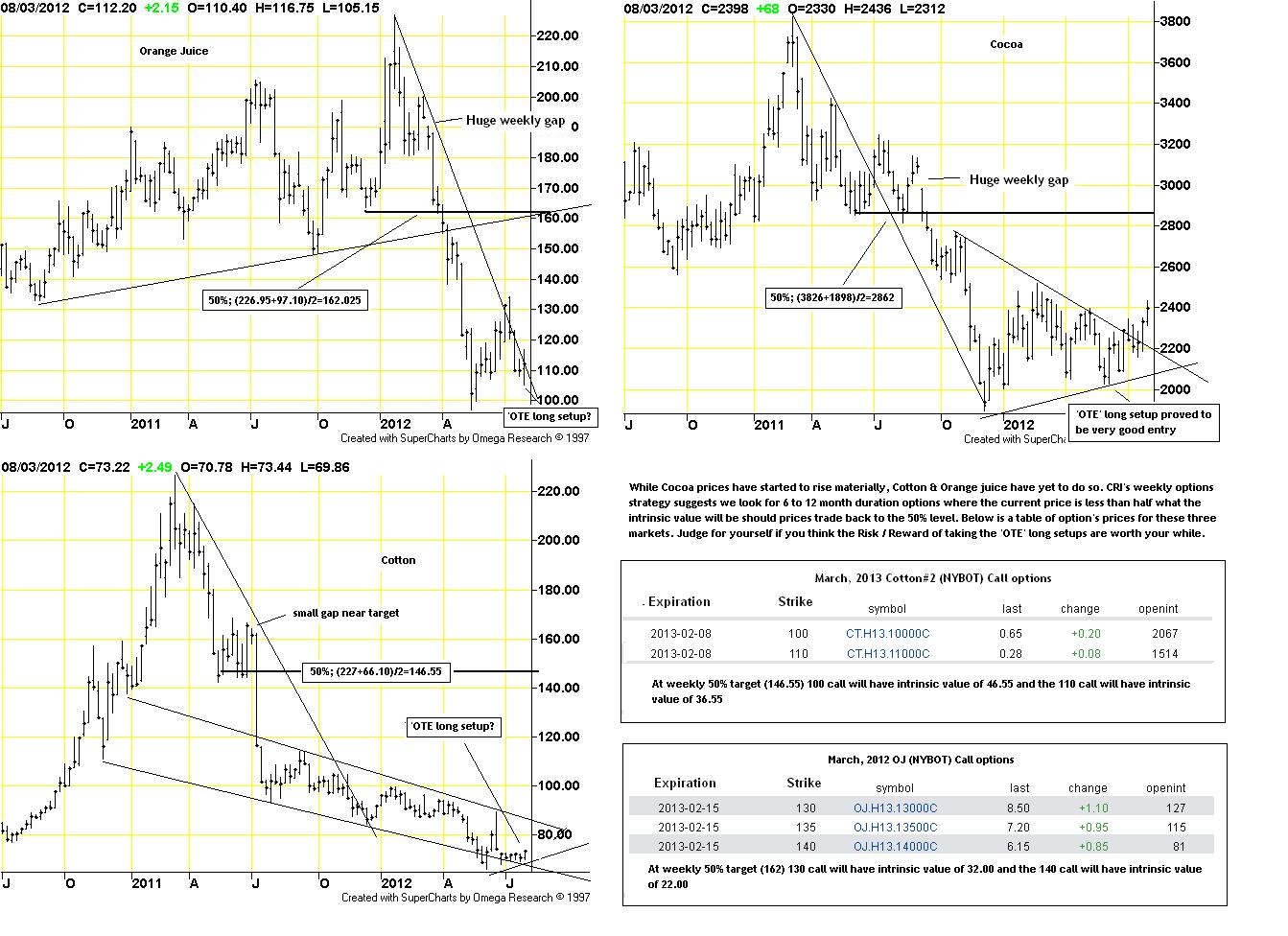

So now on to the chart. The first thing that jumps at me is the fact that the 50% level is almost 40 points higher than where we are now. Yet the recent lows are only 20 points lower. That would represent a 2:1 risk reward model. Addtionally, this market is current within both the 2 year and 1 year 'OTE' zones suggesting again that the risk/reward model is tilted towards the reward side.

I would advise taking some time over the coming week to look seriously at 6-12 month call options (on your most favored ETF proxy....for me probably the XIU March, 2013 $17 call currently $1.05 offered TMX link or about twice what I want). If I can find one where the price paid today is half (or less) what the intrinsic value of the option will be should prices move to the 50% level, I might just pull the trigger - seems like an interesting OnlyDoubles trade, no????

That's all for this issue of the CTS Spotlight,

Brian Beamish FCSI

the_rational_investor@yahoo.com

the_rational_investor@yahoo.com