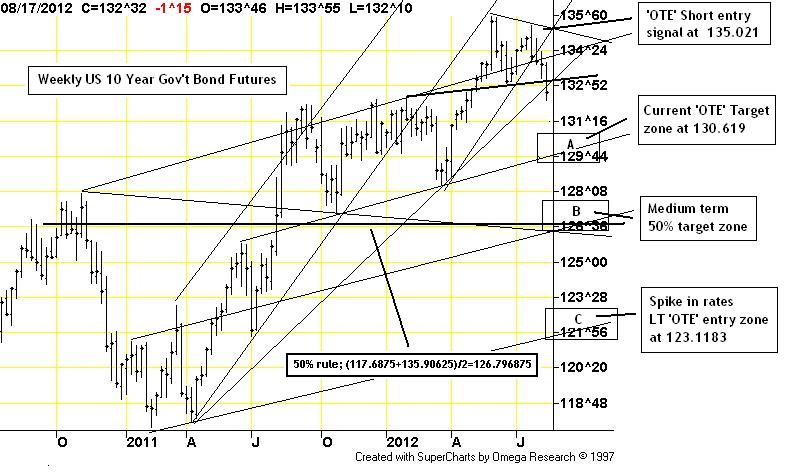

Now that we are officially into the month of May one should be very cautious for the next six weeks. Historically, many commodity related business\'s use May as a seasonal pivot (where supply and demand influences peak) so one shouldn\'t be too surprised to see wild gyrations through this transitional period. Since we know most of the world\'s equity markets are very overextended I am troubled by what I see developing in the long end of the yield curve (see WCTS Blog post). It would appear bonds are starting to look more attractive relative to stocks. Couple all this with the turmoil out of Eastern Europe and I for one shall be reluctant to commit new money to ideas for a while yet.

As we fast approach the typical seasonal top for the North American economy it shouldn't surprise us to see the anti-equity-market proxy (bonds) start to look more attractive. While I am not suggesting a trade (low reward to risk ratio on setup prevents me from considering the idea) , I do respect the fact that we may see a nice rally from current levels. Three justifiable reasons suggest to me price wants to revisit the low 140 area in the not too distant future. 1. Inverted Head and shoulders price pattern target (outlined on chart). 2. Optimal Short Trade Entry (OTE) zone currently about 144 to 148 [keep in mind, institutions do not short down markets, this is the area that they will look to short to play this bear market - not near the lows here]. 3. Gaps near 143 & 145 need to be filled. Put it all together and I can comfortably understand a bond market rally - but as previously mentioned, because reward is about equal to risk I simply can not justify taking a trade....

That's all for this issue of the WCTS Spotlight,

Brian Beamish FCSI

The Canadian Rational Investor

the_rational_investor@yahoo.com

http://www.therationalinvestor.ca/RI_Tradents.php#wctsspotlight

http://www.therationalinvestor.ca

That's all for this issue of the WCTS Spotlight,

Brian Beamish FCSI

The Canadian Rational Investor

the_rational_investor@yahoo.com

http://www.therationalinvestor.ca/RI_Tradents.php#wctsspotlight

http://www.therationalinvestor.ca